ADVERTISEMENT

The FY 2016 Financial Future: How the Cath Lab Impacts the Hospital Bottom Line

Kristin Truesdell is a Decision Support Manager with Corazon, Inc., offering strategic program development for the heart, vascular, neuro, and orthopedic specialties. Corazon offers a full continuum of consulting, software solution, recruitment, and interim  management services for hospitals, health systems, and practices of all sizes across the country and in Canada.

management services for hospitals, health systems, and practices of all sizes across the country and in Canada.

To learn more, visit www.corazoninc.com or call (412) 364-8200. To reach the author, email ktruesdell@corazoninc.com.

Hospitals are currently in a challenging predicament: changing regulations and intense scrutiny of proper reimbursement, along with pressure to reduce costs and both measure and achieve high-quality outcomes, is transforming the way care is provided across all clinical service lines. And, it’s no wonder that cardiovascular (CV) services are at the forefront of administrator’s minds, as the specialty is one of the most significant services lines in a hospital — meaning, a CV program has the potential to bring high-volume and high-revenue procedures to a hospital, but of course, not without high cost. Balancing this with the aforementioned requirements is no easy task.

Corazon continually remains on the leading edge of payment updates and other important financial trends, and we believe it is imperative that hospitals are prepared for what is to come, well in advance of the effective date of any changes. The following summary provides a high-level look at the upcoming fiscal year (FY) 2016 changes in terms of financial and quality standards. Understanding these updates can help hospital and program leaders, along with the cath lab staff, to be aware of new criteria and  how the changes, either major or minor, impact the hospital’s bottom line.

how the changes, either major or minor, impact the hospital’s bottom line.

Payment updates

Inpatient payments

Under the Centers for Medicare and Medicaid Services (CMS) FY2016 hospital inpatient final rule, the market basket update is 2.4% for acute care hospitals; however, hospitals will only see a net increase of 0.9% in overall operating payment rates due to adjustments. These adverse adjustments include the following:

1. Documentation and Coding Adjustment = 0.8% decrease. This adjustment was implemented in FY2008 when CMS converted the Diagnosis Related Groups (DRG) system from CMS-DRGs to MS-DRGs. CMS plans to continue this adjustment until $11 billion is recovered from hospitals between 2014 and 2017 due to past overpayments.

2. Productivity Adjustment = 0.5% decrease. This adjustment was implemented in FY2012 to address economic productivity.

3. Accountable Care Act (ACA) Adjustment = 0.2% decrease. This adjustment was implemented in FY2011 to address the needs of the ACA and healthcare cost savings. CMS plans to continue this adjustment until FY2019, unless changes are made after the November 2016 presidential election.

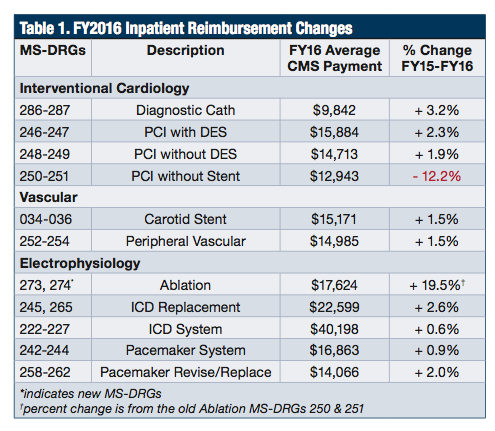

Even though hospitals lost 1.5% in operating payments due to adjustments, facilities should still realize a gain in inpatient reimbursement rates over the last fiscal year. Table 1 highlights a comparison of payments from FY2015 to FY2016 for the most common inpatient cath lab procedures. With the exception of “PCI without Stent”, ALL cath lab procedures will receive an increase for inpatient payments.

In addition to the overall increases in cath lab reimbursement, CMS also deleted two MS-DRGs and added seven new MS-DRGs to further define major cardiovascular surgical procedures, ablations, and aortic and heart assist procedures.

Deleted

• MS-DRG 237–Major Cardiovascular Procedures w/MCC

• MS-DRG 238–Major Cardiovascular Procedures w/o MCC

Added

• MS-DRG 268–Aortic & Heart Assist Procedures Except Pulse Balloon w/MCC = $37,086

• MS-DRG 269–Aortic & Heart Assist Procedures Except Pulse Balloon w/o MCC = $23,053

• MS-DRG 270–Other Major Cardiovascular Procedures w/MCC = $27,958

• MS-DRG 271–Other Major Cardiovascular Procedures w/CC = $18,556

• MS-DRG 272–Other Major Cardiovascular Procedures w/o MCC/CC = $13,290

• MS-DRG 273–Percutaneous Intracardiac Procedure w/MCC = $20,961

• MS-DRG 274–Percutaneous Intracardiac Procedure w/o MCC = $14,288

Previously, ablations were embedded in PCI without stent MS-DRGs 250 and 251, which yielded an average reimbursement of $14,747 in FY2015. But after years of suggested comments, and considerations of costs and other clinical factors, CMS finally realized the differences in resource utilization. By separating ablations from PCIs without stents, hospitals will see a gain of approximately $3,000 for an ablation case vs previous years.

Outpatient payments

Since close to half of today’s cath lab procedures are paid as outpatients, payments for this population must be critically reviewed. Based on the proposed rule released by CMS in July 2015, CMS continues to aggressively shift outpatient payments to a true prospective payment system.

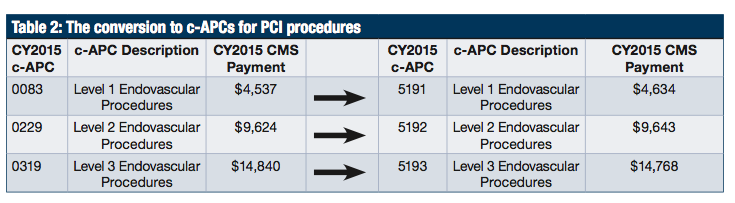

Initiated in the CY2015 final rule, CMS furthers the move towards Comprehensive Ambulatory Payment Classifications (c-APCs). Comprehensive APCs combine a number of procedures required to support the delivery of the primary service into a single all-inclusive payment, with no additional reimbursement for affiliated procedures performed during the same operative session. Last year, CMS focused on restructuring all high-cost device-dependent APCs (i.e., stents) into c-APCs. To further CMS’s long-term goal of a packaged outpatient system, nine new c-APCs are proposed, as well as a complete renumbering system of the c-APCs. Hospitals are still required to append the status indicator “J1” to specify the c-APC. Table 2 illustrates the conversion and payment differences for PCI procedures.

Now that a year has passed, the two-year change between payments for the c-APCs for PCI procedures is minimal. Level 1 endovascular procedures saw the only increase in payments with 2% growth, whereas Level 2 remained constant, and Level 3 had a decrease of 0.5%.

In addition to the vascular cases that are also included in the Level 1-3 endovascular c-APCs, CMS is also proposing further changes to electrophysiology procedures.

Quality updates

In order to realize maximum reimbursement potential, hospitals must adhere to the three quality standards noted below or else receive a reduction in base payments. For hospitals with poor quality performance, the FY2016 increases in reimbursement for cath-lab based procedures will easily be overshadowed by penalties.

Readmissions

The Hospital Readmissions Reduction Program requires a reduction to a hospital’s base operating DRG payment as a means to account for excess readmissions of selected applicable conditions. Of the five existing conditions (acute myocardial infarction, heart failure, pneumonia, chronic obstructive pulmonary disease, total hip arthroplasty, and total knee arthroplasty), only pneumonia was refined to expand the measure cohort.

Value-Based Purchasing (VBP)

The estimated base operating DRG payment amount reductions for FY2016 (1.75%) is the same amount available for value-based incentive payments, which is approximately $1.5 billion overall. Although the measures for FY2016 were finalized in previous rulings, including 24 measures, CMS has made final and proposed rulings for the future VBP program. CMS is adding a care coordination measure beginning with the FY 2018 program year and a 30-day mortality measure for chronic obstructive pulmonary disease beginning in the FY 2021 program year. CMS is also removing two measures, effective with the FY 2018 program year.

Hospital-Acquired Conditions (HAC)

As part of the Affordable Care Act, a 1% reduction in payment is being made to hospitals whose ranking is in the lowest performing quartile. In this final rule, CMS added two surgical site infection measures following colon surgery and abdominal hysterectomy, as well as expanded the data definition for catheter-associated urinary tract infection (CAUTI) and central line-associated blood stream infection (CLABSI). In FY2017, expect inclusion of incidence rates for MRSA infection and clostridium difficile infection.

Corazon recommends that hospitals pay close attention to quality data for the current year, especially because as standards shift, current outcome trends will help to determine whether a hospital will be penalized or incentivized in the future.

Other notable updates

Two-Midnight Rule

As published in the final FY2016 inpatient rule, CMS made no changes to the current rule, but states it will be addressed in the hospital outpatient ruling. In the proposed CY2016 outpatient rule, CMS proposed that for stays that a physician expects to last less than two midnights, an inpatient admission would be acceptable on a case-by-case basis, depending on the judgment of the physician and the documentation justifying the stay. CMS will monitor short-stay admissions and prioritize them for medical review. Currently, the rule has been delayed until December 2015, which prohibits Recovery Audit Contractors (RAC) from conducting post-payment patient status reviews for claims with dates of admission from Oct. 1 through Dec. 31, 2015.

In addition, CMS also realized that Medicare Administrative Contractors (MAC) is likely not the best equipped to handle this controversial issue; therefore, responsibility has shifted to Quality Improvement Organizations (QIO). The two-midnight rule is expected to be finalized in the CY2016 outpatient final rule.

Corazon advocates that hospitals proactively evaluate the financial impact of the two-midnight rule and understand the details of patients with one-day length of stays. Corazon’s proven model calculates the impact of this rule not only from a revenue standpoint, but also from the cost of resources. For example, a hospital with a total of 100 cases with length of stays between 1.0–1.9 days can expect a decrease in payments of approximately $500,000 if the two-midnight rule is implemented — a significant impact! Strategies for ways to offset these decreases will be necessary in the coming months, as this change is more likely to become a reality.

ICD-10 implementation

Anxiety is setting in for all healthcare providers, as it seems that CMS is standing strong for ICD-10 implementation on October 1, 2015. ICD-10 will affect diagnosis and inpatient procedure coding for everyone covered by the Health Insurance Portability Accountability Act (HIPAA), not just those who submit Medicare or Medicaid claims. Claims for services provided on or after the compliance date should be submitted with ICD-10 diagnosis codes. And, claims for services provided prior to the compliance date should be submitted with ICD-9 diagnosis codes. CMS has taken steps to promote awareness and education by providing free action plans, education, webinars, references, and support on their website. Corazon recommends accessing these resources now as a last effort to ensure preparedness in the face of this change.

Impact summary

The final rulings go into effect October 1, 2015 for the inpatient payment system and January 1, 2016 for the outpatient payment system. Savvy hospital and program leaders should always give close attention to the reimbursement for the cardiovascular service line, as changes to this specialty and included sub-specialties can have a major impact on the bottom line for both the specialty and the hospital overall.

Based on this summary, Corazon recommends that all hospitals pay close attention to the financial and quality performance of their CV service lines, the cath lab in particular. Though many of the FY2016 changes are positive, implementing efforts to maintain consistent cardiovascular profit margins can favorably impact the overall organizational bottom line, despite decreases in other areas. An initial look at the financial, operational, and quality processes can reveal areas needing improvement and/or areas of opportunity. Any potential opportunity to improve performance should be considered a priority moving forward, as the healthcare financial environment will no doubt continue to evolve, for better or for worse.